Warning

I am not a finance professional, or a tax expert, or anything of the sort. I am NOT here to tell you how to invest your money. If that was why you came, sorry. I will only be discussing how I plan to invest my own money over the next year.

I will explain my overall investment style and then what changes I’ll make based on Trump taking office again. This post will probably be my longest yet, and I don’t expect anyone to read it start to finish, so I will try to make each section self-contained.

TL;DR - This is not investment advice. I won’t really be changing much in what I do with my money. I learned the dangers of being too active in the market the first time Trump was in office.

My investment style

I am intentionally not calling this “my investment strategy”, because that would imply this is some kind of long-term plan, something with a specific goal in mind that I’ve back tested, and know produces returns in the long run. This ain’t that.

This is basically how I run my own money and essentially what allows me to stay in the market, no matter what craziness is going on. I think to fully appreciate it, I’d have to tell you about my investment history starting in 2012, BUT I’m not going to do that now, perhaps another post.

Because of how active I like to be in the market I realized it’s best for me to have multiple accounts. I have a Roth IRA, a traditional IRA, a pure brokerage account, and a YOLO account. These different accounts give me greater flexibility in what I can invest in and take into account the different time frames I have for my investments.

For my Roth account the idea is “it’s time in the market, not timing the market”. From everything I’ve learned about investing from reading the experts to just being in the market, it seems like the best way to make money is to invest in an index fund, keep on adding and then go along for the ride. Therefore, in this account I typically put some money in every year and invest in the following index funds1:

VOO - Mirrors the S&P500

VGT - Mirrors the tech heavy QQQ

VIG - Mirrors the old school Dow30 companies

The main idea is to buy shares of these various index funds every month with the assumption that I won’t be selling any shares for 20 to 30 years. If the VOO is down 5% and I’ve got the cash on hand, I’ll buy more shares than usual, with the assumption that it’ll just go back up. The hope is that by buying more in the short term when it’s down, in the long-haul, I can slightly edge out the market.

I don’t divide my money equally into the three index funds. The VGT, tech-heavy one gets more money now because I’m trying to be more aggressive while I can, and then eventually I’ll shift so the investments are going to the more traditional “blue chip” companies and thus put it more into VIG. As for performance of this account, I want to note that the S&P returned 24% last year2 and my Roth was around 25%.

For my traditional IRA account, I have about a 1 to 3 year time frame in terms of how long I’m willing to hold a stock. This account is smaller than my Roth account and I don’t even add funds to it every year. This account was created from 401ks that I had to transfer out from my previous jobs. Whereas my plan with the Roth is to just buy and hold indexes, here I allow myself to buy and sell individual companies. But they are “solid” ones like AAPL, MSFT, CVS, PFE, etc. You get the picture.

To not kick myself for buying at the highest high and selling at the lowest low, I have adopted a method where I always hold small amounts of any of these companies all the time. For example, let’s say in 2025 I like AAPL, for whatever reason. Then I will plan to build a position of about 30 shares. As I do this, my goal is to get the best price available at that time, so waiting a day here or there, but within a week I need to add to the position. Once I get all 30 shares, then I just wait. If the investment is up 20%, I start taking some shares off and get down to about 5 shares. I’ll keep this small portion and then start to size back up. I can’t say this idea works all too well, my returns for 2024 were about 11%. The S&P did about 24%, so I got beat by more than 2X. Ouch.

So why do I still keep this account? For one, I like the discretion that it gives me, and it’s smaller than my Roth so I’m inherently risking less, while having some fun and learning more about the markets by actively participating. Or at least that’s what I’m telling myself.

Next up I’ll discuss my pure brokerage account. I like to call this my speculation account (spec acct). I have 100% discretion on when to buy and sell. It doesn’t matter if the investment is up, down, or range bound. If I’m holding because I can’t give up on a trade or trying to hold something while it goes to the moon. That’s what this account is for.

Because of intentional volatility of this account it’s smaller than my IRA account. It’s also smaller because I’ve made a ton of mistakes betting on things like Z, ABNB, and IRNT, and lost money. I’m not adding money into this account. It is what it is. If it eventually gets ground down to zero, then that will be the most explicit lesson in “time in the market” (Roth acct) vs “timing the market” (spec acct).

I don’t even think I want to report my percent gain/loss for this one last year. I’m pretty sure it was negative, so I’ll leave it at that. Besides trading any stock, IPOs or whatever, I also trade futures in this account. For a variety of reasons, I don’t trade options. But if I did this would be the account where it happened.

Finally, my YOLO account. This account is exactly what it sounds like. My gambling account. The smallest of the four and meant for things that even the spec account can’t get to as easily. This is the account where I trade crypto, and try to get shares of a stock before it even IPOs. That’s worked out for me once (DUOL). The other times (VAXX, SEV) I did it, I held for too long, and each of them have become penny stocks.

This account went up 65% in 2024. Why don’t I just YOLO my retirement accounts then? Well it’s because this account has on occasion also been down 50 to 80%. Remember Crypto-winter? The biggest reason it’s up so much this year is BTC going up 125% in 2024. And DOGE is up around 312%. Both skyrocketing after Trump got elected. Yes, I own DOGE. That’s the point of this account. To get in on all the memes and “stonks” and such stupid trends and make money or have fun. It’s gambling.

So that’s my current investment style. Having done it for a little over a decade, I know myself well enough to create outlets for over-managing positions in the Roth account and giving up gains. Therefore, I have the other accounts, while holding the majority of my retirement savings in the Roth using the boring yet effective, index fund approach.

What happened last time…

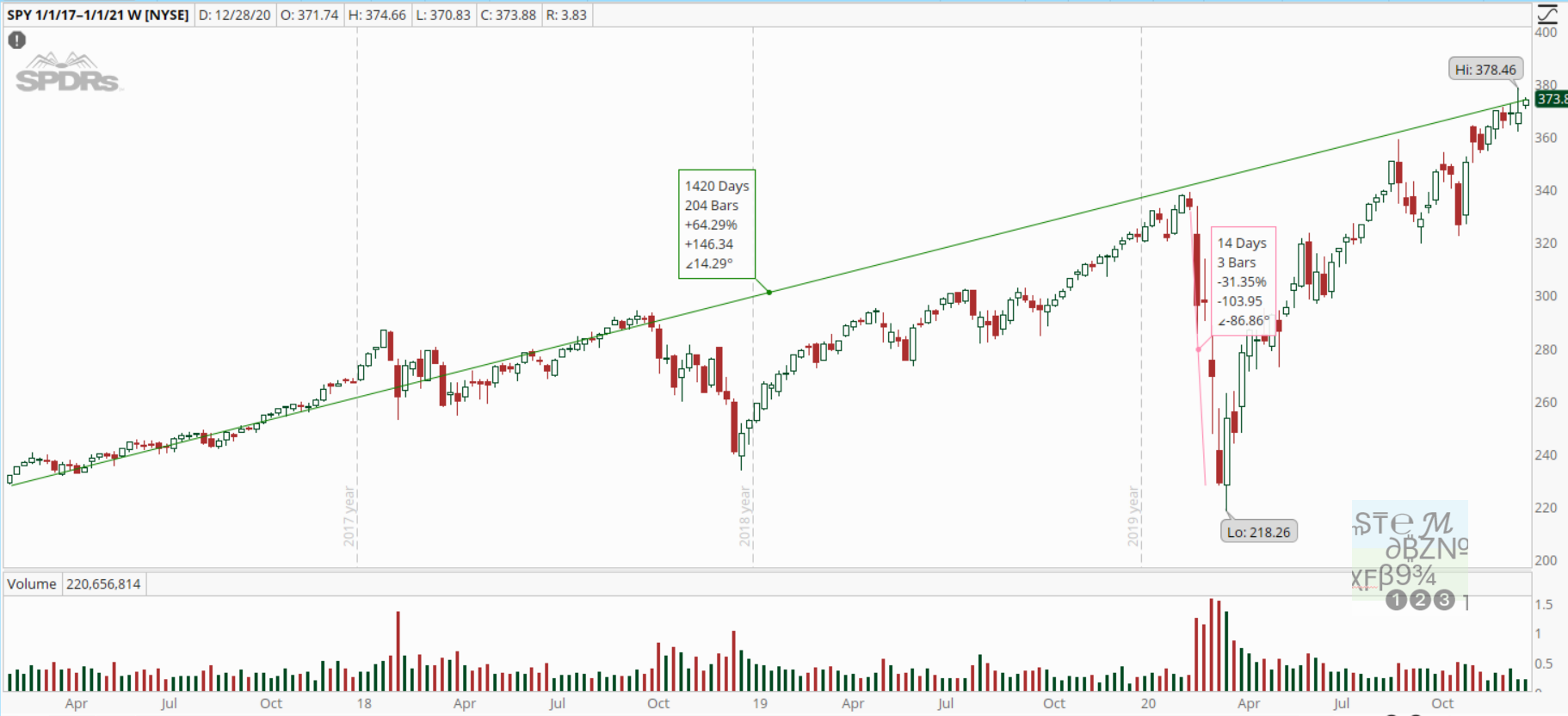

The chart above is for the S&P 500 from Jan 1st, 2017, to Jan 1st, 2021, where each “candle” shows the weekly change. Trump didn’t technically take or leave office during these dates, but I think it’s the simplest way to measure return while he was president. Even though the S&P 500 is not the entire market it is a good proxy for measuring overall market returns.

So last time, the index started at 220 and then got to 340 by Jan 2020, but we all know what happened next: COVID. That’s the big 31% drop in 14 days. By March of 2020 the market was pretty much exactly back to 220, when Trump took office. Returning nearly ZERO pct in three years! However, the market made a dramatic comeback in a few months reaching a 4-year high, and by Jan 1st, 2021, was at 373, which makes the return in this time period around 62%.

To be extra clear, if you had invested $1,000 in the S&P index on Jan 1st 2017 and then sold all of it Jan 1st 2021, you’d have $1,620. Looking at this chart and having been in the market during this time tells me one thing.

Boring is better

That’s right, just be boring and buy an index fund or two and walk away. If you can add to the fund every month or year, great, you’ll get an even higher return in the long run. The point is just to buy in and hold.

I had to learn this the hard way of course. When Trump first took office, I thought the market was going to implode due to all his craziness, and sure there was volatility but nothing major really changed. But I pulled out a bunch of money in my 401k and kept it in cash. Getting panicked by Trump and the seemingly imminent war with Iran or North Korea. But the market wasn’t panicked, it would swing up and down but essentially just kept humming along. Then I felt like I was being left behind, got back in around Oct 2018, and the market dropped 20%. Yup.

I didn’t learn my lesson, so I waited for the market to get me back to break even and then pulled out a bunch again. As in 2018 the market just kept going up. I got frustrated and thought, screw it, this market just goes up no matter what. I’ll just go all in, and I added funds around Feb 2020. And then COVID! I was watching the news out of China and Italy, I knew what was going on, I worked in the sports industry, and I still didn’t think to get conservative with my investing. Dumb, dumb, dumb!

Of course I can say all of this with hindsight. What I’ve really learned is that it’s better to just be boring, get an index fund and let the returns come in. Given that I can’t always keep myself on this “correct” but boring path, I have my smaller accounts where I can play and try my best to time the market.

But I don’t like it

If you can’t make yourself do the boring thing, and I truly get it, you can look into exchange-traded-funds or ETFs. An ETF is very much like an index fund, but instead of tracking 500 companies (SPY) it will track 20 to 30-ish, based on certain criteria. For example, DDD or PRNT are ETFs that track a variety of 3-d printing companies. So, if you want to invest in that space, but aren’t sure of which company, and/or want to expose yourself to less risk, you can invest through the ETF to track all the 3d printing companies. At least all the ones on the stock market and held by that specific ETF.

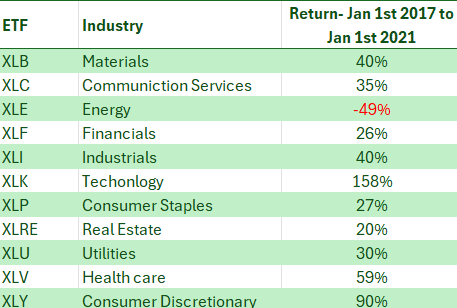

Needless to say, there are thousands of ETFs to choose from, but I like to invest in SPDR sector-based3 ETFs , for example XLC is for Communications services industry, XLE is for Energy. Let’s say for some reason you think energy stocks (Exxon, Chevron, etc.) will do well under Trump, but don’t want to invest in these individual companies, then you can buy into XLE and wait.

Last time around here is how those ETFs performed:

Just remember “historical performance is not an indicator of future results”, or as day traders like to say “the trend is your friend, till the end”. That being said, XLE doesn’t actually look like where I’m going to put my money, I will probably stay focused on XLK, but if tariffs drive inflation, that would hamper those returns. But who really knows?!

No, I really don’t like it!

ETFs still too boring? Well, you could be like me and invest/trade directly in individual stocks. Or even more exciting and wild: Crypto.

Let’s talk Crypto first, BTC has been going wild since Trump took office, and I don’t see why his policies would negatively affect the Crypto market. In fact, given the tech-bros that he’s surrounding himself with, and getting advice from, I can see favorable Crypto related policies being proposed but I don’t know if they get passed. I always like to keep in mind that Crypto is a very volatile market, not just to trade in, but in general. Remember the implosion of FTX? I’m not thinking about Crypto as money for retirement, it’s just fun to be part of the ride.

I don’t know why but ETH has not enjoyed as much of a gain due to Trump, but “shit-coins” that no one has heard of are doing well, so it’s hard for me to make sense of it all. I’m basically sticking with BTC, ETH, and DOGE. That’s right, going to keep buying DOGE, because not only is it cheap and ridiculous, there is actually going to be a Department of Government Efficiency (D.O.G.E) which Elon Musk certainly did on purpose as he has pumped the price of DOGE before, and I expect him to do it again. Not to mention, algos that trade off of Tweets or Xs or whatever they are called, will probably pick up chatter about D.O.G.E. which will affect the price of DOGE, so yeah.

As for individual stocks, back to Elon Musk. TSLA has been doing great since Trump got elected, and I think it will continue. I also know that Trump and corruption go together like mac & cheese, so I’m also looking at DJT, Trump’s social media company. I have a handful of shares in my YOLO account with the idea that sovereign wealth funds of Saudi Arabia and other countries will use that as a mechanism to buy Trump. OR Elon will simply buy out the company with the billions he’s making from TSLA stock going up, as a kiss-up to Trump and to help himself by taking out a competitor to X.

I hope you are judging me for trying to make money off rampant corruption. I judge me too, I honestly stayed away from DJT, thinking there is going to be a lawsuit about it and I don’t want to even be on the periphery of something like that. I thought about shorting it and donating the gains to the DNC. I didn’t because that would have been an emotionally driven trade and even with YOLO, I try to stay away from that, I’ve learned.

You see, I didn’t buy into FB/META when they took that huge dump in Oct 2018 or during COVID because I thought, I didn’t want to be part of their money making machine which is destabilizing the world, and hurting vulnerable people like the Rohingya refugees4. I got on a moral high horse and what happened. Nothing. FB is still FB and in the meantime I just “lost” a trade that would have made 50 to 60%. This isn’t to say I still won’t bring my morality into my trades. refuse to trade gun stocks.

The last individual stocks I’ll talk about are PYPL, PLTR and RBLX. The reason I’m invested in PYPL is because I’m stuck holding it from COVID times, but I’m adding to it because Peter Thiel used to own PYPL, and he is going to be influential in the Trump admin. Given his deep ties to JD Vance there is no way he’s not getting involved. Thiel is also a co-founder of PLTR which was up 340% in 2024, making it the best performing stock of the S&P last year. I’ve traded it before, but I hate the idea of the company, so I didn’t buy and hold. Morality losses strike again, I suppose. I currently don’t have any shares of PLTR but will be keeping an eye on it.

RBLX is a stock I do trade and hold shares in the YOLO account. As such it’s mostly for fun, but all I hear from my kids, and their cousins, and from other parents is Roblox! And how all the kids want for X-mas is Roblox gift cards so they can use them to make in-game purchases. Who knows where this will go, but if the kids like it, and the parents are buying the gift cards (and I am), then it’s probably a good bet regardless of Trump.

Final thoughts

If the individual stock picks has you nervous, that’s good. It’s a risky proposition and maybe now you are thinking about really boring, safe and risk-free gains. If that’s the case, I see no reason to not buy CDs or bonds yielding between 4 and 5%, if you can find them. Inflation probably isn’t going to head to 2% this year and might just be stuck at 3% for a while. Which means if you can find a risk-free 5% return, your money is at least growing at 2%.

Assuming Trump goes in on day one and tries to tariff Mexico, Canada, China, Denmark, and on-and-on, that will eventually translate to higher prices for the US consumer, a-la-inflation. All the Nobel laureate economists who are predicting this trajectory could be wrong, but I’m going to bet they aren’t. This would mean tech stocks might suffer, like they did last time inflation was a big issue, so I am cautiously adding to my tech holdings.

In general, I think the issue of inflation is probably way bigger than Trump and the US economy writ large. The entire world experienced COVID and the inflation that ensued is also a world-wide phenomenon. If I have more thoughts on this topic, I’ll write more.

For now, let me just say again, none of this post should be mistaken for investment advice. But if you are not in the market, I would recommend you start “doing your own research”, and start thinking about investing. And while it’s pretentious, class-ist, and smacks of nationalism, it’s been said the US stock market is the greatest generator of wealth…I couldn’t agree more.

I used to have money in the cash-backed index ETFs, SPY, QQQ, and DIA, but I think the Vanguard ETFs have a lower expense ratio and every bit helps.

https://www.schwab.com/learn/story/it-was-very-good-year

https://www.sectorspdrs.com/

https://www.amnesty.org/en/latest/news/2022/09/myanmar-facebooks-systems-promoted-violence-against-rohingya-meta-owes-reparations-new-report/